Plastribution’s Polymer Price Know-How: December 2024

|

Getting your Trinity Audio player ready...

|

Plastribution’s December Polymer Price Know-How discusses how the market is still heavily influenced by weak demand and supply-demand imbalances. The stronger USD continues to exert cost pressures on polymers imported from outside Europe, while European prices remain constrained by low purchasing activity. Polyolefin prices remain stable, with limited movement, while styrenics and recycled polymers reflect ongoing challenges in maintaining inventory levels amid subdued market activity. As the industry prepares for seasonal shutdowns, 2025 is expected to bring fresh developments, including potential price adjustments and structural changes within the sector.

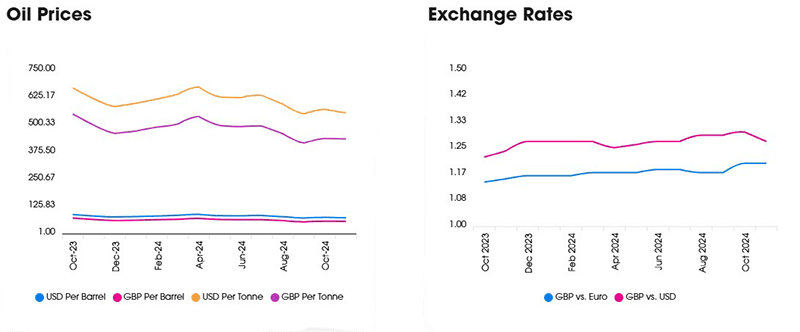

Whilst a $0.03 increase in the value of the USD against both the GBP and Euro should drive cost inflation both directly for polymers sourced from outside Europe, which are typically priced in USD, and indirectly through feedstock costs for European petrochemical producers, where Crude Oil is priced in USD, the stark reality is that supply demand balance is of paramount importance.

From the viewpoint of polymer buyers, it matters little whether the weakness is resulting from lower monomer costs or stiff competition for scant polymer orders. The extent of price movements is polymer specific and, with the exception of some rollovers on tighter and more specialist grades, the tendency is still towards lower prices throughout November and into December.

The start of 2025 is expected to be dynamic as demand returns to normal, following the seasonal converter shutdowns in December and as polymer suppliers contemplate price increases in order to improve beleaguered margins.

Exchange Rates

€- 1.20

$- 1.27

€/$- 1.06

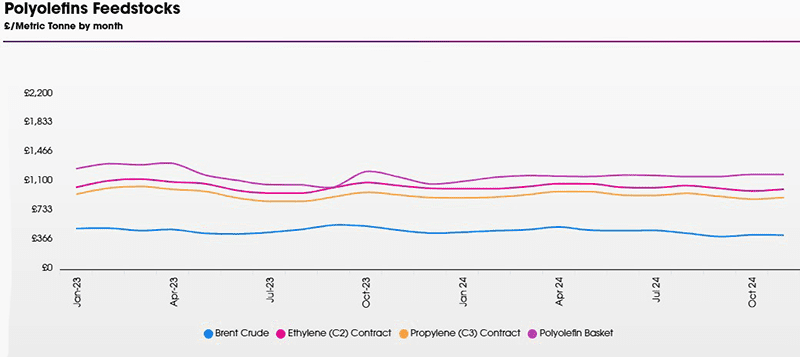

Polyolefins

Polyolefin prices are mostly rolling over in December, with some grades under a little bit of downward pressure.

Whilst Ethylene C2 and Propylene C3 both reduced by €7.5 / MT and €10 / MT respectively, many producers are not agreeing to pass these on as they swallowed much bigger monomer increases in November. Demand continues to be poor and consequently, there are some deals available from traders.

Outlook for the New Year is for a rollover to begin with and then some strengthening of prices around February. Producers can’t keep making losses indefinitely so at some point, there will be a change in approach. 2025 could be a volatile year with potential plant closures and further rationalisation in the European industry. Add to that some uncertainty with potential new tariffs on major trade flows, with possible impacts on freight rates and availability, we could be in for a rocky period.

Styrenics

Contract EU Styrene prices fall, cancelling small rise from previous month. EU polymers are looking steady.

Styrene monomer has fallen by just €7/T, settling at €1408/T.

For December, EU GPPS, HIPS and ABS either rolled prices or followed the small drop.

GPPS/HIPS/ABS supply chains are running at reduced rates, no doubt triggered by low demand. Converters and distributors are running inventory at very low levels due to financial pressures. Therefore, any adjustments in polymer prices are likely to be passed on immediately.

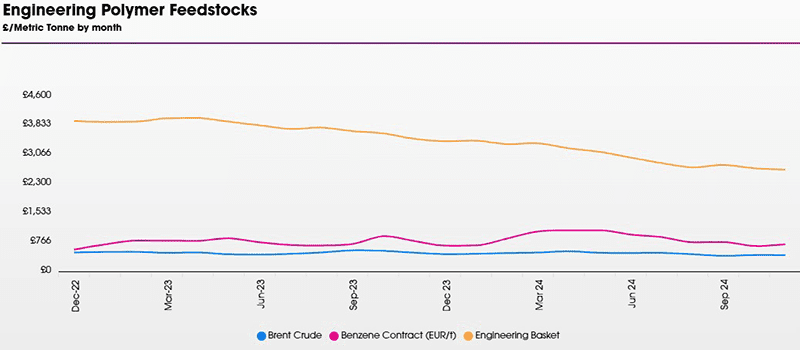

Engineering Polymers

December is traditionally a shorter month, however it is anticipated that the year will end abruptly as producers cutback on production and start maintenance programs.

Demand remains extremely poor across most materials and market sectors. Inventories are heavily stocked and prices continue to drop for most polymers.

The December benzene contract has settled €49/Mt lower than November at €812/Mt.

Sustainable Polymers

Recycled Polyolefins have mostly rolled over in December alongside prime prices.

It remains to be seen how much impact recent closures of recycling plants in the UK will have on availability and pricing, but at the time of writing, supply still appears to be good and demand still quite weak.

There have been some suggestions that many organisations involved in producing cosmetics packaging are demanding more high quality natural recycled HDPE & PP to meet their sustainability goals.

Recycled LDPE / LLDPE

Recycled LDPE / LLDPE has mostly rolled over in December.

High-quality grades continue to see strong demand and restricted availability leading to prices keeping above virgin.

Recycled PP

Recycled PP is rolling over in December though pressure remains on industrial grades with continued poor demand in key sectors.

As with other recycled grades, high quality natural commands a strong premium over virgin.

Recycled HDPE

Recycled HDPE is typically rollover with industrial grades continuing to be under pressure with lower than hoped for demand in construction and other key markets.

Natural grades for consumer packaging continue to see significant premiums over virgin prices.

Price Know-How: December 2024 Full Report

Visit the Price Know-How website to read the December 2024 update, which details each market segment and material group produced by Plastribution’s expert product managers.

Subscribe and keep in the know.

Price Know-How, a decade-long trusted resource in the industry, provides essential updates on polymer pricing and market dynamics. This report is crafted by Plastribution, a leading polymer distributor, in collaboration with Plastics Information Europe.

Price Know-How is tailored specifically for the UK polymer industry, unlike many other price reports. They do all the currency conversions, so you don’t need to!

Please click here to subscribe for free and receive monthly updates directly to your inbox.

Read more on Plastribution here.